By Abbas Merchant, Aible Industry Advisor

It’s no exaggeration to say that the pandemic has turned our personal and professional lives upside down.

Prior to the pandemic, most of our focus was on relationships, improving ourselves and self-actualization. Now we have to contend with things that many of us have long taken for granted: safety, good health, earning a living, and taking care of family.

It’s no wonder that consumer tolerance for sales and marketing pitches is very low and that many financial institutions have cut their sales and marketing budgets. Last year’s marketing plans describe a world that no longer exists. We have to quickly refocus on new realities -- away from marketing and sales and towards our employees’ and customers’ needs.

Three key consumer trends in banking are important right now:

- Consumers are shifting their behavior from going to the branches to banking from the safety of their homes, either by phone/video or using self-service capabilities

- Consumers are looking for easier ways to meet their needs and the ability to do it on their own time

- The definition of home has changed. Home is serving multiple purposes that go well beyond a place for resting and relaxing. Home has become an office, a daycare center, a school, a senior care center, and much more.

Most homes are not set up to adequately meet the new realities. This has created a demand for home renovation and improvement to better equip homes to meet these needs. Traditionally, proximity to the workplace has been an important factor when buying a home, but this is becoming less important, leading to renewed interest in suburban and rural communities.

As consumer behavior is changing, so too are financial institutions.

During the initial months of the pandemic, FIs turned their focus on business continuity – ensuring employee safety, reducing branch hours, relying more on drive-through, digital channels to offset the temporary branch closures or limiting branch servicing to pre-scheduled appointments. At the same time, they began to figure out how best to meet the evolving needs of consumers – the disbursement of PPP loans, forbearance, and working with customers to allay their concerns and anxieties.

Most FIs have had to accelerate their technology transformation in order to develop end-to-end capabilities for servicing, especially for tasks that used to be done in person. That means consumer perceptions about their FIs are being shaped by how well financial institutions support their needs during the pandemic. How easy was it to get PPP or have financial questions answered? Did my financial institution show empathy and act with my financial needs in mind?

This is likely to create churn among the FIs that are not able to meet the evolving needs of their customers. And it creates an acquisition opportunity for institutions that are more customer-centered.

Let’s take a closer look at some emerging opportunities.

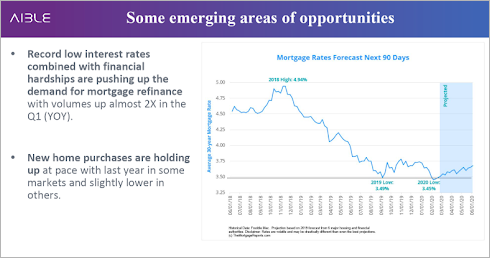

Most FIs have significantly reduced their prospecting activities and focused more on cross-sell. We’re seeing record refinance volumes, driven by 20-year interest rates at record lows. New home sales are holding up, while credit card and loan originations are gaining ground after the lows of the past few months.

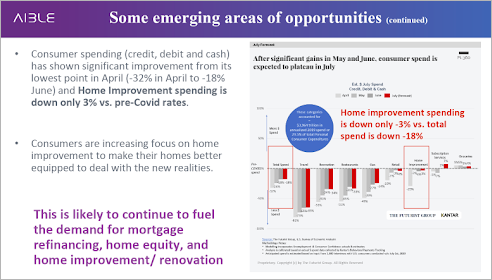

Cumulatively, these trends are likely to increase consumer spending on home improvement and continue to spur greater demand for home equity and refinancing activities.

The impact of the pandemic will continue to vary by geography, creating pockets of opportunities in some markets and shutdowns in others. Financial institutions need to be nimble to address the opportunities that are on the top of consumers’ minds. As consumer preferences change, so must the FIs.

During turbulent times, past performance is less and less a predictor of future success. The problem is, most of our targeting models, product mix, offers and our entire marketing plans are based on what has worked in the past. So how do we use data to make prudent market decisions in the midst of uncertainty? How do we evaluate multiple scenarios?

The best approach is Augmented Intelligence – combining human domain knowledge with the best of Artificial Intelligence.

Augmented Intelligence can help marketers manage three key analytics challenges in the new business reality. Call them: What, So What, and Now What.

What – The efficacy vs. simplicity paradox

We know that we can improve the efficacy of our targeting models by developing multiple segment-specific models. However, this can exponentially create complexities in deploying multiple models and trying to execute on them. Many times, businesses compromise by settling for much more generalized models.

So What – To determine the optimal mix, you have to consider cost-benefit tradeoffs and resource constraints

Many of the marketing models are designed to optimize response or conversion. But not all customers are equally profitable. This again leads marketers settling for a good enough outcome or applying broad assumptions that are imprecise but get the job done.

Now What – How do we anticipate change, and then test and learn and repeat?

The COVID-19 challenges can’t be met by AI or humans acting alone. Combining human domain knowledge and AI is the best way to identify strategies that are more robust and have greater likelihood of being successful. With humans and AI working together, we can leverage data insights, while also being more nuanced about optimizing for business impact and reacting to change faster.